The late-1990s tech bubble (a.k.a. the dot-com era) is one of the market’s greatest magic tricks: it made otherwise sensible adults believe that (1) profits were optional, (2) “eyeballs” were a currency, and (3) adding “.com” to a business name could legally replace a business plan.

And here’s the part investors still wrestle with decades later: the bubble didn’t just hurt people who bought at the top. It changed the math of future returns for years. In fact, the real lesson of the tech bubble isn’t “technology is risky.” The lesson is: price matters more than a great storyand paying too much can turn a revolutionary decade into a disappointing one for your portfolio.

What “Tech Bubble” Really Means (Hint: It’s Not Just a Tech Problem)

A bubble happens when prices sprint far ahead of fundamentalsrevenue, cash flow, realistic growth, and what humans call “basic arithmetic.” In the dot-com period, technology was the spark, but the fuel was a familiar mix: easy money, hype, fear of missing out, and the belief that the old rules had retired to Florida.

The bubble coincided with real innovation: the internet was spreading fast, productivity looked strong, and capital flooded toward anything that seemed “internet-shaped.” That combinationgenuine progress plus speculative pricingis why bubbles are so persuasive. They’re not pure fiction. They’re fiction with a few true facts sprinkled on top, like chocolate chips in a cookie… except the cookie costs 80 times earnings.

The Crash in Numbers: When Gravity Re-Introduced Itself

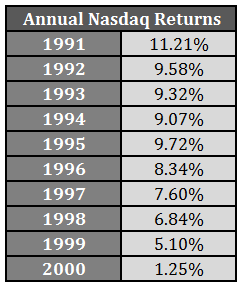

The dot-com bubble peaked in early 2000 and then unraveled in spectacular fashion. The tech-heavy NASDAQ fell dramatically from its March 2000 high to its 2002 low, wiping out years of gains and a whole lot of confidence. It wasn’t a normal “bad quarter.” It was a multi-year reminder that markets can be ruthless about expectations.

Meanwhile, broad U.S. stocks went through what many investors call the “lost decade.” Even diversified investors holding a mainstream large-cap benchmark saw a stretch where returns were far weaker than the 1980s and 1990s had trained them to expect.

The economic knock-on effects mattered too. Policymakers noted that the decline in stock values erased massive wealth and likely contributed to weaker conditions going into the early-2000s recession. A bubble bursting doesn’t only rewrite portfoliosit can reshape sentiment, spending, hiring, and risk appetite.

Why Bubbles Wreck Future Returns: The Not-So-Fun Math

1) Starting valuation quietly sets the “speed limit” for returns

Future returns come from a small handful of sources: business growth, dividends (or cash returned to shareholders), and changes in valuation (how much investors are willing to pay per dollar of earnings or cash flow).

In a bubble, that last piecevaluationgets stretched like taffy. When you buy at extreme prices, you’re borrowing returns from the future. The market has already priced in years (sometimes decades) of amazing outcomes. That leaves less upside and more ways to be disappointed.

A simple thought experiment:

- If a company earns $1 per share and trades at $20, investors are paying 20× earnings. If earnings grow to $2 and the multiple stays 20×, the price could be $40. Nice.

- If that same company trades at $100 (100× earnings), it can still be a fantastic business… and still be a terrible investment if the multiple later falls to something normal.

That’s the bubble trap: you can be right about the technology and wrong about the return. The dot-com era produced world-changing companies, but it also produced world-class overpayment.

2) Mean reversion is the market’s version of “we need to talk”

Valuations don’t stay extreme forever. When investor optimism fades, multiples compresssometimes gently, sometimes like a folding chair. If the price you paid assumed perfection, the market doesn’t need a disaster to hurt your returns. “Slightly less perfect than expected” is often enough.

This is why valuation measures like the Shiller CAPE ratio (a cyclically adjusted price-to-earnings metric) are often discussed in the context of long-term expected returns. The point isn’t that CAPE predicts next month. It’s that starting valuation tends to influence the next 10–15 years more than people want to admit when excitement is high.

3) Bubbles increase the chance of long “recovery timelines”

Many investors assume that if a company keeps growing, the stock price will “eventually” catch up. Sometimes it does. But “eventually” can be long enough to feel like a historical reenactment.

One famous dot-com-era example is Cisco. The company remained a real business with real products and substantial revenue, but the stock’s dot-com valuation was so extreme that it took roughly a quarter-century to fully surpass its 2000 peak. That’s not a knock on the company; it’s a lesson about paying the wrong price.

Survivors, Casualties, and the Danger of “Only Remembering the Winners”

When people talk about the dot-com era today, they often point to survivors: Amazon, Microsoft, and other enduring giants. That’s trueand it’s also a sneaky cognitive trap called survivorship bias.

The bubble era also produced a long list of blowups and near-misses: businesses with shaky economics, thin margins, and business models that depended on capital markets staying generous forever. When funding dried up, many firms didn’t merely decline; they vanished.

The key point for future returns: bubbles don’t just change prices. They change which companies exist a decade later. That makes “buy the hottest theme” strategies especially risky: the theme can be right while many of the theme’s stocks are… not.

The “Lost Decade” Effect: How One Bubble Can Haunt a Whole Portfolio

The dot-com crash didn’t only punish speculative tech stocks. The broader U.S. market experienced a long stretch where returns were unusually weakpartly because the starting point (late-1999 valuations) was rich, and partly because the 2000s delivered multiple hits: the bubble bursting, recession, and later the global financial crisis.

For long-term investors, this matters because the market doesn’t grade you on storytelling. It grades you on outcomes. A decade of flat-to-negative returns can be manageable if you’re steadily contributing and rebalancing. But it can be devastating if you needed those returns on a specific timeline (retirement, college, major purchase).

What the Dot-Com Bubble Teaches About Future Returns (Without Predicting the Future)

Lesson 1: “Great company” and “great investment” are not synonyms

A great company can be overpriced. A mediocre company can be underpriced. Stocks are not trophies for spotting innovation; they are claims on future cash flows. Future returns depend on what you pay versus what you get.

Lesson 2: The market is terrible at timing which business models win

Even policymakers acknowledged the difficulty of identifying which technologies and business models would prevail over decades. In bubbles, that uncertainty gets papered over by confidence. Then reality shows upuninvitedand changes the return equation.

Lesson 3: Concentration risk grows when “the winners” become everyone’s portfolio

Bubbles often concentrate market leadership into a narrow set of names. That can inflate index returns in the short run, but it also increases vulnerability. When leadership narrows, diversification matters more, not less.

Practical Ways to Defend Future Returns When a Theme Is Red-Hot

1) Diversify like you mean it

Diversification is not a buzzword; it’s damage control. Investor education resources routinely emphasize the “don’t put all your eggs in one basket” logic for a reason: a single theme can underperform for years, even if it changes the world. Spreading exposure across sectors, styles, and geographies can help keep any single mania from dominating your outcome.

2) Rebalance (a.k.a. sell a little of what got expensive)

Rebalancing forces a simple discipline: trim what’s run up and add to what’s lagged. In bubble conditions, it’s one of the few ways to systematically reduce exposure to stretched valuations without pretending you can call the top.

3) Separate “innovation exposure” from “valuation surrender”

You can invest in technology without buying the frothiest names at the frothiest prices. Consider broad funds, quality screens, profitability filters, or simply position sizing: keep speculative allocations small enough that a drawdown is annoying, not life-altering.

4) Match your time horizon to your risk

If you need the money in two to five years, bubble-priced assets are a terrible place to store it. If you have 20+ years, you can survive volatilitybut you still can’t escape valuation. High starting prices can mean lower long-run returns, even over long horizons.

5) Be skeptical of narratives that delete the word “competition”

In the dot-com bubble, the internet was realbut competition was also real. When a gold rush starts, most people don’t get rich from gold. They get rich from selling shovels… and sometimes even the shovel sellers get overpriced. Future returns depend on who keeps pricing power and margins once the crowd arrives.

Conclusion: The Bubble’s Lasting Impact Is a Valuation Lesson

The tech bubble’s most enduring legacy isn’t that technology is dangerous. It’s that overpaying is expensive. The dot-com era proved that revolutionary change can coexist with brutal returns if investors price the future too aggressively today.

If you want to improve your odds of strong future returns, focus on what bubbles distract you from: valuation, time horizon, diversification, and discipline. Innovation will keep coming. The market will keep getting excited. Your job isn’t to avoid excitementit’s to avoid overpaying for it.

Investor Experiences & Lessons From the Dot-Com Era (About )

Ask investors who lived through the dot-com era what it felt like, and you’ll often hear two stories that sound like they happened on different planets. The first story is the party: coworkers swapping stock tips at lunch, brand-new IPOs doubling on day one, and the sense that owning “old economy” companies was like using dial-up internet on purpose. People watched portfolios climb quickly and started doing the most dangerous thing an investor can do: mentally spending gains that weren’t realized yet.

Then comes story number two: the hangover. Many investors recall watching once-beloved tech names slide 10% in a day, then 10% again, and againuntil the question shifted from “How high can it go?” to “Does this company still exist?” Some learned, painfully, that broad market indexes can recover faster than a concentrated basket of hot stocks, because indexes quietly replace losers with new winners over time. A single-stock portfolio doesn’t get that helpful housekeeping.

Retirement savers had their own version of the experience. Plenty of 401(k) participants were heavily allocated to large U.S. growth funds because that’s what had worked in the 1990s. When the market entered a rough stretch, some stopped contributing or moved to cash after losseslocking in the damage. Others kept buying through the downturn. Those steady contributors often describe a counterintuitive benefit: when prices were lower, each contribution bought more shares. The recovery didn’t feel good while it was happening, but consistency improved long-term outcomes.

Employees paid in stock or stock options experienced a special kind of emotional roller coaster. During the boom, paper wealth made people feel wealthier than they were; during the bust, falling share prices sometimes changed career plans, home purchases, and even where people chose to work. Many later adopted a personal rule: if your paycheck and your portfolio depend on the same company, you’re taking “double exposure” riskso it’s wise to diversify outside your employer when you can.

There were also investors who “picked right” on technology but still felt disappointed. They bought strong businesses, held through volatility, and watched the companies growyet returns lagged for years because the starting valuations were too high. That experience forged one of the most valuable investing instincts: it’s not enough to be right about the direction of the world. You also need a price that leaves room for reality to arrive on schedule.

Put all these experiences together and you get a practical takeaway: bubbles don’t just test your portfolio; they test your behavior. The investors who came out best rarely had perfect foresight. They had diversification, position sizing, and the willingness to keep a long-term plan when the market’s mood swings tried to negotiate a new one.