Note: This article is for general financial education only, not personalized investment advice. Your ideal stock market time horizon depends on your goals, cash needs, risk tolerance, tax situation, and overall financial plan.

Investing in the stock market can feel a little like planting a tree and then checking every 11 minutes to see if it has become a forest. Stocks need time. Not because Wall Street enjoys suspense, but because businesses grow, earnings compound, markets wobble, recessions happen, recoveries surprise everyone, and investors who can stay patient often give themselves a better chance of capturing long-term returns.

So, how long should your time horizon be in the stock market? A practical answer is this: money you may need within the next three years generally does not belong heavily in stocks. Money needed in three to five years should be invested cautiously. Money with a five- to ten-year horizon can usually accept moderate stock exposure. Money you will not need for ten years or longer is often better suited for a diversified stock-focused strategy.

That does not mean stocks are magic. They are not. Stocks can fall fast, stay down longer than expected, and make even calm investors talk to their portfolio like it owes them rent. But time is one of the strongest tools investors have, because a longer investment horizon gives the market more room to recover from downturns and gives compounding more room to do its quiet, powerful work.

What Is a Stock Market Time Horizon?

Your stock market time horizon is the length of time you expect to keep money invested before you need to use it. It is not just your age. It is not simply how optimistic you feel after reading a headline about artificial intelligence, interest rates, or “the next big thing.” It is the timeline attached to a specific financial goal.

For example, a 28-year-old saving for retirement may have a 35- to 40-year time horizon. That same 28-year-old saving for a house down payment in two years has a very short time horizon. Same person, different goal, different strategy. This is why smart investing starts with the question, “When do I need the money?” rather than “Which stock is going to the moon?” Rockets are exciting. Rent, college tuition, and retirement income are more demanding.

Why Time Horizon Matters So Much in Investing

Stocks have historically offered higher long-term return potential than cash and many high-quality bonds, but that potential comes with volatility. In plain English: stocks can reward patience, but they can also throw tantrums. The shorter your time horizon, the more dangerous those tantrums become.

If you need money next year and your portfolio drops 25%, you may be forced to sell at a bad time. That is not investing; that is financial arm wrestling with a bear market. But if you do not need the money for 20 years, a downturn may be unpleasant rather than disastrous. You still need discipline, diversification, and a plan, but you are not under the same pressure to sell immediately.

Time horizon also affects asset allocation, which is the mix of stocks, bonds, cash, and other investments in your portfolio. Longer horizons often support a higher allocation to stocks. Shorter horizons usually call for more cash, Treasury bills, certificates of deposit, money market funds, short-term bonds, or other lower-volatility options.

A Practical Guide: How Long Should You Stay Invested?

0 to 3 Years: Keep It Safe and Liquid

If you need the money within three years, the stock market is usually not the best parking lot. It is more like a roller coaster with a “no refunds” sign. Short-term goals may include an emergency fund, a wedding, a car purchase, a home down payment, taxes, tuition due soon, or cash needed for a business expense.

For this time horizon, the priority is not maximizing return. The priority is preserving capital and keeping money accessible. Cash, high-yield savings accounts, money market funds, Treasury bills, and short-term certificates of deposit may make more sense than a stock-heavy portfolio. You might earn less, but you reduce the chance of needing your money right after the market takes an unexpected nap on the floor.

3 to 5 Years: Be Careful With Stock Exposure

A three- to five-year time horizon is tricky. It is not exactly tomorrow, but it is not “see you in 2045” either. Some investors may hold a modest stock allocation for goals in this range, but the portfolio should usually lean conservative. The reason is simple: market downturns can last long enough to interfere with medium-term plans.

Suppose you are saving for a home purchase in four years. Putting all the money in stocks could work beautifully if the market rises. It could also backfire if a bear market appears right before you need the cash. A more balanced approach might include a large allocation to cash or high-quality short-term bonds, with only a small stock component if you can tolerate volatility and have flexibility in your timing.

5 to 10 Years: A Balanced Approach Often Makes Sense

With five to ten years, investors may have enough time to accept some stock market risk, but not so much time that they can ignore volatility completely. This range often fits goals like a child’s future college expenses, a planned home upgrade, a sabbatical, or early retirement bridge money.

A balanced portfolio may include diversified stock funds, bond funds, and cash reserves. The exact mix depends on flexibility. If your goal date is firm, such as college tuition beginning in a specific year, you may want to reduce stock exposure as the date approaches. If the goal is flexible, such as buying a vacation property only when conditions are favorable, you may be able to accept more volatility.

10 Years or Longer: Stocks Become More Reasonable

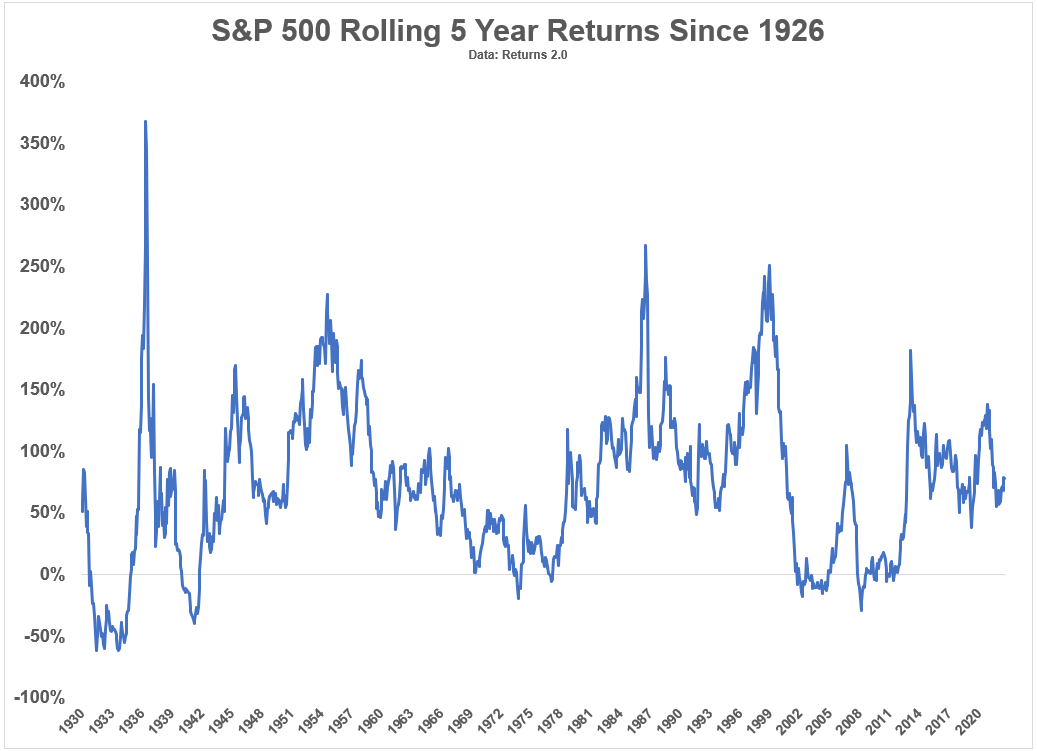

For a time horizon of ten years or more, stocks often become a more reasonable part of the portfolio. Historically, longer holding periods have reduced the chance that an investor experiences a negative return, although they never eliminate risk. A 10-, 20-, or 30-year horizon gives businesses time to grow, dividends time to reinvest, and compounding time to become the quiet overachiever in the room.

This is why retirement investors in their 20s, 30s, and 40s often hold stock-heavy portfolios. They are not doing it because they enjoy volatility. They are doing it because long-term goals usually require growth, and stocks have historically been one of the most effective tools for pursuing that growth.

Time Horizon and Risk Tolerance Are Not the Same Thing

Time horizon tells you how long your money can stay invested. Risk tolerance tells you how much volatility you can emotionally and financially handle. You need both. A long time horizon does not automatically mean you should be 100% in stocks if every market dip makes you want to sell, hide under a blanket, and swear off capitalism until Tuesday.

Risk tolerance has two sides. The first is financial capacity: Can you afford losses without damaging your life? The second is emotional capacity: Can you stay invested when your portfolio is down? A portfolio only works if you can live with it during bad markets, not just admire it during bull markets.

For example, two investors may both have 25 years until retirement. One may feel comfortable with 90% stocks. Another may sleep better with 70% stocks and 30% bonds. The “best” portfolio is not always the one with the highest expected return. It is the one you can stick with long enough for the strategy to matter.

Market Timing Is Not a Substitute for Time Horizon

Many investors ask, “Is now a good time to invest?” That is understandable. Nobody wants to invest right before a downturn. Unfortunately, consistently predicting market tops and bottoms is extremely difficult. The best and worst trading days often occur close together, especially during periods of high volatility. Investors who sell during panic may miss powerful rebound days.

A healthier question is, “Does this money have the right time horizon for stocks?” If the answer is yes, then a diversified, disciplined strategy often beats waiting forever for a perfect entry point. If the answer is no, then even a market that looks attractive may be too risky for that specific money.

Dollar-cost averaging can help investors ease into the market by investing a fixed amount at regular intervals. It does not guarantee profits or prevent losses, but it can reduce the emotional pressure of investing a lump sum all at once. For long-term investors, the bigger lesson is that time in the market usually matters more than trying to make every entry point perfect.

Specific Examples of Matching Goals to Time Horizons

Example 1: Emergency Fund

An emergency fund should usually not be in stocks. If the car breaks down, the roof leaks, or your dog decides to eat something that requires a veterinarian and a small personal loan, you need cash immediately. The correct time horizon is “right now,” which means safety and liquidity matter more than return.

Example 2: House Down Payment in Two Years

A future homebuyer saving for a down payment in two years should generally avoid heavy stock exposure. A market decline could delay the purchase or force the buyer to accept a smaller down payment. High-yield savings, Treasury bills, CDs, or short-term conservative investments may be more suitable.

Example 3: College Savings in Eight Years

A parent saving for college expenses eight years away may use a balanced approach. Stocks can provide growth potential, but the allocation should likely become more conservative as tuition gets closer. Many education savings strategies use a glide path that gradually reduces risk over time.

Example 4: Retirement in 30 Years

A worker with 30 years until retirement can usually consider a stock-heavy diversified portfolio, assuming risk tolerance supports it. Over decades, short-term volatility becomes less important than long-term growth, consistent contributions, low costs, diversification, and the ability to stay invested.

Example 5: Retirement Already Started

Retirees still need a time horizon, but it becomes layered. Money needed in the next one to three years may belong in cash or short-term reserves. Money needed later in retirement may still need growth assets to fight inflation and support a retirement that could last 25 or 30 years. Retirement is not the end of investing; it is a new chapter with stricter cash-flow rules.

How to Adjust Your Portfolio as Your Time Horizon Shrinks

Your time horizon is not frozen in amber. It changes. A 15-year goal eventually becomes a 10-year goal, then five years, then “the tuition bill is due and apparently colleges do not accept good intentions.” As the goal gets closer, your portfolio should usually become more conservative.

This gradual adjustment is often called a glide path. Target-date retirement funds use this concept by holding more stocks when the target date is far away and gradually shifting toward bonds and other conservative assets as the date approaches. You can apply the same idea to your own goals by reducing volatility as the spending date becomes clearer.

Rebalancing is also important. If stocks perform well, your portfolio may become riskier than intended. If stocks fall, your allocation may become too conservative. Rebalancing brings the portfolio back to its target mix, helping you buy low, sell high, and avoid letting market movement secretly rewrite your plan.

Common Mistakes Investors Make With Time Horizon

Mistake 1: Investing Short-Term Money in Long-Term Assets

The biggest mistake is putting money needed soon into volatile investments. A vacation fund, tax bill, or down payment should not be treated like a retirement account. The market does not care about your closing date.

Mistake 2: Being Too Conservative With Long-Term Money

The opposite mistake is keeping long-term money entirely in cash. Cash feels safe, but inflation can quietly reduce purchasing power over time. For goals decades away, avoiding all market risk may create another risk: not growing enough.

Mistake 3: Changing Strategy Based on Headlines

Headlines are designed to get attention, not build your retirement plan. Interest rates, elections, recessions, technology trends, and global events matter, but constantly changing your allocation based on news can lead to emotional decision-making. Your time horizon should be the anchor.

Mistake 4: Forgetting Taxes and Fees

Time horizon also affects taxes and costs. Frequent trading can create taxable events and transaction costs. Long-term investing, especially through low-cost diversified funds, may help reduce unnecessary friction. A portfolio is not just what it earns; it is what you keep after expenses, taxes, and preventable mistakes.

How Long Is “Long Term” in the Stock Market?

In everyday conversation, “long term” can mean anything longer than a weekend without checking your phone. In investing, long term usually means at least ten years. A truly long-term stock market time horizon may be 15, 20, 30, or even 40 years.

That said, no number is perfect. Stocks can disappoint over a decade. Valuations, inflation, interest rates, corporate earnings, and investor behavior all influence returns. A long time horizon improves the odds of success, but it does not guarantee a smooth ride or a specific result.

The better approach is to build a margin of safety into your plan. Keep short-term money safe. Diversify long-term money. Add consistently. Rebalance periodically. Avoid panic selling. Review your plan when your life changes, not every time the market sneezes.

Personal Experiences and Practical Lessons From Real-Life Investing Behavior

One of the clearest experiences investors often share is that their actual time horizon feels much shorter during a market decline. On paper, someone may say, “I am investing for 25 years.” Then the market drops 20%, financial news turns dramatic, and suddenly that 25-year plan emotionally shrinks to about 25 minutes. This is normal. It is also why a written investment plan is so useful. When emotions get loud, the plan can speak in a calmer voice.

Consider an investor who begins contributing to a retirement account every month at age 30. During the first bear market, the account balance falls even though contributions continue. That feels discouraging. But the investor who understands time horizon sees something different: shares are being purchased at lower prices, and the retirement goal is still decades away. The downturn is uncomfortable, but it does not automatically break the strategy.

Now compare that with someone saving for a house in two years. If that person invests the down payment aggressively and the market drops, the experience is very different. There may not be enough time to recover. The buyer may need to delay the purchase, reduce the budget, or borrow more. This is not a failure of the stock market. It is a mismatch between the investment and the goal. Stocks were asked to do a short-term job they were never designed to do.

Another common experience involves investors who wait for the “perfect” time to invest. They watch the market rise and say it is too expensive. Then it falls and they say it is too scary. Then it recovers and they say they missed it. This cycle can continue for years. A long time horizon does not require perfect timing. It requires a reasonable strategy, steady contributions, and the humility to admit that no one gets a calendar invitation before every market rally.

Many experienced investors eventually learn that behavior matters as much as selection. A simple diversified portfolio held for decades can outperform a complicated strategy that the investor abandons at the worst possible moment. The best investment plan is not the flashiest one. It is the one that matches the goal, fits the time horizon, survives bad markets, and lets the investor sleep without refreshing stock quotes at midnight.

There is also a confidence-building effect that comes with time. Investors who live through multiple market cycles often become less reactive. They remember that downturns feel permanent while they are happening, but many have historically been followed by recoveries. They also learn that every bull market eventually looks obvious in hindsight and terrifying in real time. Patience is not passive; it is an active decision to let a good plan work.

The practical lesson is simple: separate your money by purpose. Keep near-term spending money safe. Invest medium-term money with caution. Let long-term money pursue growth. Your stock market time horizon should not be based on hope, hype, or the mood of the market. It should be based on when you need the money and whether you can stay invested through the inevitable rough patches.

Conclusion: Your Time Horizon Should Match Your Goal

So, how long should your time horizon be in the stock market? Ideally, at least five years for meaningful stock exposure and ten years or more for a stock-heavy strategy. Shorter than that, caution becomes more important. Longer than that, growth and compounding become more powerful allies.

The stock market is not a savings account with better lighting. It is a long-term wealth-building tool that works best when paired with patience, diversification, realistic expectations, and a plan you can actually follow. If your goal is near, protect the money. If your goal is far away, give your investments room to breathe. And if the market gets noisy, remember: your time horizon is the steering wheel. Headlines are just passengers yelling from the back seat.