Note: This article is for educational purposes only and is not financial advice. It synthesizes real public information from major U.S. investment research, endowment reporting, index-investing education, and 2020 market commentary without inserting source links.

Introduction: When “Smart” Investing Gets Too Clever

In investing, “simple” has a public-relations problem. It sounds basic. Ordinary. Like ordering plain toast at a brunch place that serves lavender-honey ricotta pancakes. Complex investing, on the other hand, sounds sophisticated. It wears a blazer. It says things like “non-correlated return streams” and “illiquidity premium” before breakfast.

But the 2020 edition of the simple vs. complex investing debate gave investors a useful reminder: complicated does not automatically mean better. During a year shaped by the COVID-19 market crash, emergency monetary policy, huge swings in equities, and unusual stress across public and private markets, many simple diversified portfolios held up better than expected. Meanwhile, some complex institutional portfoliosespecially those modeled after large university endowmentshad to manage not only returns, but liquidity, spending needs, committee politics, private-fund commitments, and a small mountain of paperwork that could probably stop a door in a hurricane.

The phrase “Simple vs. Complex, 2020 Edition” points to a larger question: should investors favor a clean, low-cost, easy-to-rebalance portfolio, or should they chase the more elaborate endowment-style approach filled with hedge funds, private equity, venture capital, real assets, and alternative strategies?

The answer is not “simple always wins” or “complex is always bad.” That would be too easyand investing rarely hands out gold stars for lazy thinking. The better answer is that complexity must earn its keep. If a portfolio is harder to understand, more expensive, less liquid, and more difficult to rebalance, it should offer clear benefits. Otherwise, it may be financial theater with a fee schedule.

What “Simple” Means in Investing

In this discussion, a simple portfolio usually means a broadly diversified, low-cost index fund strategy. A classic example is the three-fund portfolio, often associated with Bogleheads and inspired by Vanguard founder John C. Bogle’s philosophy. The idea is beautifully plain: own the broad U.S. stock market, the broad international stock market, and the broad bond market.

The Three Core Ingredients

A simple three-fund portfolio commonly includes:

- A total U.S. stock market index fund

- A total international stock market index fund

- A total U.S. bond market index fund

That is it. No secret handshake. No exclusive lunch with a hedge fund manager named Chad who says “alpha” every twelve seconds. Just diversified exposure to thousands of securities across different asset classes.

The power of this structure is not that it predicts the future. It does not. A simple index portfolio will still fall when markets fall. Bonds can disappoint. International stocks can lag. U.S. stocks can have ugly decades. But the strategy focuses on what investors can control: asset allocation, diversification, fees, tax awareness, and discipline.

That last worddisciplineis the boring superhero of investing. It does not wear a cape. It rebalances once a year and goes back to sleep.

What “Complex” Means in Endowment-Style Investing

Complex investing often refers to portfolios that include alternative assets such as private equity, venture capital, hedge funds, private real estate, natural resources, distressed debt, and other strategies outside traditional public stocks and bonds. This approach is strongly associated with the Yale endowment model, which became famous for using long time horizons, illiquid assets, and manager selection to pursue higher returns.

For large institutions, complexity can make sense. A university endowment may be designed to last forever. It may have professional staff, access to elite managers, tax advantages, steady donation flows, and a long-term spending policy. A billion-dollar endowment can invest in funds that ordinary investors will never see unless they accidentally wander into the wrong conference room.

However, complex investing comes with trade-offs. Alternative assets can be less transparent. Fees are often higher. Liquidity may be limited. Private fund valuations can be reported with a lag. Rebalancing can be difficult because money may be locked up for years. And manager selection becomes critically important, which is a polite way of saying, “Good luck choosing the winners before they become obvious.”

The 2020 Endowment Reality Check

Fiscal year 2020 was a stress test with flashing red lights. The period ending June 30, 2020 included the sudden pandemic-driven crash in March, an extraordinary policy response from the Federal Reserve, a fast rebound in many public markets, and massive uncertainty for colleges and universities. Endowments were not just investing for bragging rights; they were supporting scholarships, faculty, research, operations, and emergency needs.

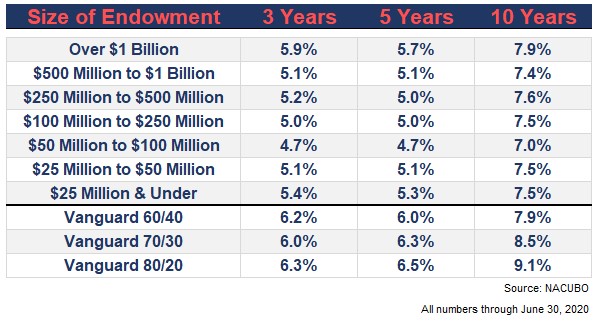

According to the 2020 NACUBO-TIAA endowment study, hundreds of U.S. colleges, universities, and affiliated foundations participated in the survey. The average endowment return for fiscal 2020 was modest compared with long-term targets, and the average institution faced an environment where spending needs rose while market conditions became unusually volatile.

This is where the simple vs. complex debate gets interesting. A low-cost index portfolio using broad stock and bond funds could be rebalanced quickly and transparently during the chaos. Endowment-style portfolios with private investments had other advantages, such as long-term orientation and reduced daily price visibility, but they also faced liquidity limits and valuation delays.

Simple Portfolios Had a Secret Weapon: Rebalancing

Rebalancing is one of the least glamorous concepts in finance. It sounds like something a dishwasher does after too many coffee mugs are loaded on one side. Yet in portfolio management, rebalancing can be powerful.

Suppose an investor starts with a target allocation: 60% stocks and 40% bonds, or perhaps 80% stocks and 20% bonds for a more aggressive long-term portfolio. Over time, market movements push the portfolio away from its target. If stocks surge, the investor sells some stocks and buys bonds. If stocks crash, the investor sells some bonds and buys stocks. This is not market timing. It is risk control.

In 2020, this mattered. After stocks fell sharply in the first quarter, disciplined investors who rebalanced were buying equities at lower prices. When the market rebounded, they benefited. Nobody knew in real time that the recovery would be so fast. That is the point. A rebalancing policy removes the need to be a financial fortune teller, which is good because most fortune tellers failed to warn us about toilet-paper shortages.

Why Low Costs Matter More Than Investors Like to Admit

Costs are not exciting. Nobody brags at a dinner party, “My expense ratio is tiny.” But in investing, small costs compound into large differences over time. A low-cost index fund strategy may not feel exclusive, but it allows investors to keep more of the return produced by the underlying assets.

Complex portfolios can carry multiple layers of costs: management fees, performance fees, fund expenses, consultant fees, legal costs, due diligence costs, and administrative overhead. For a large endowment with access to exceptional managers, those costs may be justified. For smaller institutions or individual investors, they can become a heavy backpack on a long hike.

The active-versus-passive debate is not new. Research from S&P Dow Jones Indices’ SPIVA scorecards has long shown that many active managers underperform their benchmarks over longer periods, especially after fees. This does not mean all active management is useless. It does mean the hurdle is high. If a manager charges more, trades more, and adds complexity, the manager must outperform enough to compensate for those disadvantages.

Liquidity: The Overlooked Hero of 2020

Liquidity is easy to ignore until you need it. Then it becomes very popular, like the person who remembered to bring a phone charger on a road trip.

Simple index funds and ETFs generally offer daily pricing and daily liquidity. Investors can see what they own, understand the price, and rebalance efficiently. That transparency is valuable during market stress.

By contrast, private equity, venture capital, and private real estate may lock up capital for years. These assets can be useful for long-term investors, but they are not designed for quick adjustments. If an endowment needs cash during a crisis, it may have to rely on liquid holdings, credit lines, donations, or spending-policy adjustments. Selling private investments in a hurry can be expensive or impractical.

Illiquidity also has a psychological upside. If a private fund is not priced every second, investors may feel less panic during public-market selloffs. Not seeing a price decline can reduce emotional decision-making. But not seeing the price is not the same as avoiding the loss. Sometimes the monster is still under the bed; it is just using delayed reporting.

Transparency and Control: Why Simple Is Easier to Manage

A simple portfolio is easy to explain. If a board member, spouse, client, or curious teenager asks what is inside it, the answer is straightforward: broad U.S. stocks, broad international stocks, and high-quality bonds. The holdings are diversified, public, priced daily, and relatively easy to monitor.

A complex portfolio may require more explanation. What is the current exposure to private equity? How much unfunded commitment remains? How are hedge funds valued? What happens if capital calls arrive during a downturn? Which holdings are truly diversifying, and which simply look different on a PowerPoint slide?

This does not make complex portfolios bad. It makes governance more important. A complex portfolio demands strong oversight, clear documentation, skilled staff, and a long-term commitment. Without those, complexity can become a fog machine.

When Complexity Can Be Worth It

Complexity is not the villain. Bad complexity is the villain. Useful complexity can help investors access return sources that are not available in public markets. For example, top-tier venture capital and private equity managers have historically created substantial value for some institutions. Real assets may provide inflation sensitivity. Certain hedge fund strategies may reduce portfolio volatility or protect capital in specific environments.

But these benefits are not automatic. They depend on manager access, fee terms, timing, due diligence, liquidity planning, and governance. A large university endowment may have the resources to evaluate these factors. A small nonprofit or individual investor may not.

The question is not, “Can alternatives work?” They can. The better question is, “Can this investor access the right alternatives at the right cost with the right time horizon and the right oversight?” If the answer is no, a simple portfolio may be more rational than an imitation endowment portfolio.

Simple Does Not Mean Easy

One of the great myths about simple investing is that it is emotionally easy. It is not. A three-fund portfolio is simple to build, but hard to hold during a crash. In March 2020, investors watched markets fall with shocking speed. News headlines were terrifying. Economic forecasts were gloomy. Selling felt safe, even though selling during panic often turns temporary losses into permanent ones.

Simple investing requires investors to accept boredom, uncertainty, and underperformance in certain periods. A diversified portfolio will always own something disappointing. When U.S. stocks dominate, international stocks may look useless. When stocks roar, bonds may look dull. When bonds struggle, cash may look tempting. There is always something to complain about. Diversification is the art of always being mildly annoyed for a good reason.

Lessons from the 2020 Edition

1. Strategy Beats Storytelling

Complex strategies often come with compelling stories. Private markets sound exclusive. Hedge funds sound nimble. Venture capital sounds futuristic. But storytelling is not the same as performance. A good investment strategy should be judged by net returns, risk, liquidity, costs, and the investor’s actual needs.

2. Rebalancing Works Best When It Is Written Down

Rebalancing is easy to praise and hard to execute. During a market crash, buying stocks feels unnatural. During a boom, selling winners feels foolish. A written investment policy helps investors act before emotions hijack the steering wheel.

3. Liquidity Is a Feature, Not a Footnote

The ability to raise cash, rebalance, and adjust risk matters. In calm markets, liquidity seems boring. In stressed markets, it becomes priceless.

4. Complexity Must Be Measured After Fees

A complex investment that performs well before fees but poorly after fees is like a luxury hotel that charges extra for the bed. Net results matter.

5. Governance Can Make or Break a Portfolio

Large endowments do not manage money in a vacuum. They answer to committees, boards, donors, administrators, and spending policies. The best portfolio on paper can fail if the people overseeing it panic, disagree, or misunderstand the strategy.

Simple vs. Complex for Individual Investors

For most individual investors, the simple approach has enormous practical advantages. It is understandable, inexpensive, tax-efficient when managed carefully, and easy to maintain. Investors do not need access to elite private funds to build wealth. They need a plan they can stick with.

A simple portfolio may include index funds, target-date funds, or a carefully chosen mix of ETFs. The exact allocation should depend on age, goals, time horizon, income stability, risk tolerance, and cash needs. A retiree drawing income from a portfolio needs different risk management than a 30-year-old investing for retirement decades away.

The biggest danger for individuals is not usually choosing the wrong hedge fund. It is chasing performance, selling during downturns, paying unnecessary fees, ignoring taxes, and changing strategies every time the market throws a tantrum. A simple plan helps reduce those mistakes.

Simple vs. Complex for Institutions

For institutions, the decision is more nuanced. A college, foundation, hospital, or nonprofit may have a perpetual time horizon and professional oversight. It may benefit from some alternatives. It may also need a portfolio that supports annual spending, protects purchasing power, and survives leadership changes.

The key is alignment. A complex portfolio should match the institution’s mission, spending policy, staffing, liquidity needs, and governance ability. Smaller institutions that copy giant endowments without the same access or resources may end up with complexity without the payoff.

A sensible institutional portfolio may blend simple public-market exposure with carefully selected alternatives. Complexity should be added only where it improves the total portfolio. In other words, complexity should be hired for a job, not invited because it looks impressive in a suit.

Experience Section: What 2020 Taught Real Investors About Simple and Complex

The 2020 market experience felt less like a normal investing year and more like being tossed into a washing machine with a Bloomberg terminal. Investors woke up in February with portfolios near highs, then watched markets plunge in March as the pandemic spread, businesses shut down, and uncertainty exploded. For many people, this was the first true test of whether their investment plan was a plan or just a nice spreadsheet wearing cologne.

One common experience from 2020 was the emotional advantage of simplicity. Investors who owned a few broad index funds could quickly understand what was happening. Their U.S. stock fund was down. Their international fund was down. Their bond fund might be holding steady or rising. The portfolio hurt, but it was understandable. That clarity helped some investors avoid rash decisions.

By contrast, investors with complicated portfolios often had more questions than answers. How much exposure did they really have to public equities through private funds? Were hedge funds protecting capital or quietly disappointing? Were private valuations accurate, or would losses appear later? When markets move fast, uncertainty about the portfolio can become uncertainty about the plan itself.

Another experience from 2020 was the value of having rules before panic arrives. Investors who had a written rebalancing policy did not need to guess what to do. If stocks dropped below target, they bought. If bonds grew too large as a share of the portfolio, they trimmed. The action still felt uncomfortable, but the decision had already been made during calmer times. That is the beauty of policy: it lets your rational self send instructions to your panicked future self.

Many investors also learned that “boring” assets have a purpose. Before 2020, bonds looked dull to people who wanted maximum growth. But when equities fell sharply, high-quality bonds and cash helped stabilize portfolios and provided dry powder for rebalancing. Boring became beautiful. The bond fund, previously ignored like a salad at a pizza party, suddenly had everyone’s attention.

Endowments and institutions experienced a different lesson: investment complexity must be connected to operating reality. A university portfolio is not just a return machine. It funds scholarships, salaries, research, facilities, and emergency needs. In 2020, many institutions had to think carefully about spending, liquidity, and donor restrictions while markets were under stress. A portfolio that looks elegant in a long-term model can feel very different when the institution needs cash now.

The pandemic year also reminded investors that daily pricing is both a blessing and a curse. Public index funds show losses immediately, which can create anxiety. Private assets may appear calmer because valuations update slowly. That can reduce panic, but it can also hide risk. Investors learned that volatility you can see is not necessarily worse than volatility you cannot see.

Perhaps the most important experience was that no strategy feels perfect in real time. Simple portfolios felt too exposed when markets crashed. Complex portfolios felt too opaque when liquidity mattered. Cash felt safe until markets rebounded. Stocks felt dangerous until they recovered. Bonds felt useful until investors remembered that future yields might be lower. Every choice came with discomfort.

That is why the real lesson of “Simple vs. Complex, 2020 Edition” is not that one approach permanently defeats the other. The lesson is that investors should understand what they own, why they own it, what it costs, when they can access it, and how they will behave when the market gets rude. A simple portfolio that an investor can hold through chaos may beat a brilliant complex portfolio abandoned at the worst possible moment.

Conclusion: Complexity Should Pay Rent

The 2020 edition of the simple vs. complex investing debate delivered a clear message: complexity should not be admired merely because it is complex. It should pay rent. It should improve returns, reduce risk, provide useful diversification, or solve a specific problem after accounting for fees, liquidity, transparency, taxes, and governance.

Simple investing is not perfect. It can be volatile, emotionally difficult, and occasionally disappointing. But it has powerful advantages: low costs, broad diversification, easy rebalancing, transparency, and discipline. In a year like 2020, those advantages mattered.

Complex investing can work, especially for large institutions with excellent access, long horizons, and strong governance. But copying the endowment model without endowment-level resources can be dangerous. It may add expensive complications without improving outcomes.

In the end, the best portfolio is not the one that sounds smartest in a meeting. It is the one that helps investors meet their goals and stay disciplined through uncertainty. Sometimes that portfolio is sophisticated. Sometimes it is simple. And sometimes the smartest thing in the room is the plain little index fund quietly doing its job while everyone else argues over a 300-page private placement memo.